10 steps to project success (1&2)

Steps 1 and 2: The ‘Why’ and the ‘What’

If you’re striving for more success on an important project (at home, in your job or your own business), this new series of Insights is for you.

Here I’ll share 10 fundamental steps for getting your project on the road to success…

…or cancelled as quickly as possible if it needs to be – before it costs you your job or your business!

This Insight is a 5 to 15-minute read – depending on your speed

Do you really need to know this stuff?

Just to be clear up front, this series is about how to approach real-world projects, so it won’t help you win ‘The Apprentice’ game on TV.

*That* show was certainly entertaining (and cringeworthy) at times but didn’t offer any insights into real project management which is what we’ll focus on here.

Jim Collins (Author, ‘Good to Great’) said:

Leaders of companies that go from good to great start not with “where” but with “who.”

They start by getting the right people on the bus, the wrong people off the bus, and the right people in the right seats.

And they stick with that discipline—first the people, then the direction—no matter how dire the circumstances.”

In one sense, then, this is all a business leader has to do – get the perfect team on board – and I could have saved myself a lot of writing time by saying just that.

The trouble is, perfect teams are very rare, and they’re different for each project.

So, it’s extremely valuable, whether you’re managing a project, or playing a part within one, to know what things you must have.

Then, you can spot when those things are missing, and raise your concerns or, if you’re the boss, act quickly to strengthen your team.

Oh, and by the way… exactly the same rule applies to managing your personal investment adviser.

If you learn the fundamentals of financial planning and investing, you’ll spot any big advice errors and be able to change your adviser, before it’s too late.

Education, on the fundamentals, is therefore key.

I hope you find this series useful.

My credentials – skip this if you’re familiar with my work

If you’re not yet familiar with me, I’m an escapee from the Financial Services Industry where, amongst other roles, I headed Investment Product developments for a blue-chip investment house, and directed projects that made our product set the number one sellers, in the UK.

That success was of course about having the right team around me and, on our project work, knowing how to get the best from experts across the business (across multiple locations) and outside the business too.

It was also about getting potential winner projects ‘live’ on the rails quickly, which meant working hard to kill off the many duff projects suggested to us. If you spend time exploring duff projects that others hand to you, you’ll have no time left to deliver your winners to market.

You can learn more about me here or, if you prefer following ‘gurus’, you might want to start with a detox from that habit here 😉

Better still, let’s just get on and explore what matters in the real world of projects.

Step 1. Why are you on this project?

For players in The Apprentice, this question is easy.

You work on the project, regardless of how pointless it is, for one simple reason, because Alan told you to!

In the real world, without celebrities, and on a project that might dominate your working life, not for a few hours but weeks or months at a stretch, you’ll need more motivation than that to keep going.

When you join a project, you first need to find out who’s asked for the ‘thing’ you’re going to build (a product, service, marketing campaign, whatever) and get them to explain their ‘why’.

In project speak, this person is called the sponsor, and they’re very important because they allocate the money to get the work done!

If it’s your project (at home or in your business) then you are your own sponsor.

Otherwise, the sponsor is likely to be someone senior at your work – or an external customer if you’re in the project management business.

If you don’t have a sponsor, stop work now

If there’s no named sponsor on your project, that’s a clear sign that no one really cares about it… and you might as well stop working on it – with permission from your boss of course!

If your business leaders have no interest in your project, your job is at risk if you work on it. So, get yourself onto a project they value – and do it quickly!

Have well written (and agreed) benefits statements

Having a project sponsor is a great start but do they fully understand their role?

Quite a few don’t, so, it makes sense to check that the Sponsor is very clear on the benefits expected from the project.

Some benefits are tangible, like:

- Operating cost reductions,

- New Income Streams or

- Additional Income from existing products or services.

Other benefits are less easy to define, like:

- Strategic Alignment,

- Competitive Response,

- Management Information or

- Competitive Advantage.

In particular, on business growth/marketing projects, the financial benefits are only ever estimated. So, pin some initial numbers on them, by all means, but don’t get too hung about them, just make sure the benefits are agreed and clearly stated in words.

Here, for example, are 12 benefits I’ve identified for financial advice firms considering the development of a unique, consumer-facing financial education programme – to put at the core of their marketing.

Be clear on your purpose and objectives too

Again, if your sponsor is unfamiliar with these terms, they’ll often confuse them, and that’s where you can help.

The purpose of a project, like the educational one I mentioned above, might be something like this:

(That’s my purpose for this website too, by the way!)

Objectives for a project, on the other hand, are more specific and measurable and might include things like:

- Double our Social Media follower numbers in 12 months.

- Increase our website visitor numbers by 50%, or up to a certain number, in a year.

- Increase the conversion rate from visitors/introduced prospects to clients by X%.

- Increase our client retention rate by R%.

- Increase our professional introducer numbers by Y%.

- Etc…

The key thing to check is that the project’s value is clear in the mind of your sponsor – and clearly written down too.

You might need to refer back to this document in the future; if it’s unclear, then you, or your sponsor, might be more inclined to give up on your project early on.

This ‘Purpose and Benefits’ (P&B) document has a different name in every business. ‘Project Initiation Proposal’ (PIP) is one of the less inspiring names I’ve seen!

A good project sponsor will, of course, present the project’s purpose and benefits to all the project stakeholders but, as I’ve said, some sponsors are better than others at their job.

Your first job is to get absolutely clear on what the project is all about – and your place within it.

If you’re not clear, the project and your role in the business is at risk.

Plan clearly, but be prepared to change

Now, while it’s essential to define an initial set of objectives, that doesn’t mean you’d be soft to tweak them (up or down) as the project develops.

Objectives are only estimates and provided that enough benefits look likely to survive any necessary tweaks (to scope or quality) then the project can still be viable.

The more soft-headed thing to do is to plough on with a plan that simply can’t work, and that’s, sadly, what happens on too many projects.

As a private pilot for many years, I love aviation analogies around project (and personal financial) management, and one of my favourites is about how pilots are trained to change course when they discover thunderstorms, or other unexpected hazards, en route.

The Pilot knows that they, and their passengers, would be killed if they did otherwise; thunderstorms are very violent beasts. So, make sure the same approach is taken with the project you’re on.

Accept that the destination might need to change a little.

Stay flexible – not stubborn.

I’d offer the same guidance to mountain climbers and others involved in risky pursuits, by the way. It’s often an obsessive focus on fixed goals that leads us into a disaster.

Cautious private pilots have a saying that:

I’d rather be on the ground, wishing I was flying, than flying and wishing I was on the ground.

Climbers would do well to drill a similar expression into their minds, though I understand the effort involved in climbing is much higher and the opportunities to climb Everest, very rare.

Anyway, it’s certainly worth listening to Oliver Burkeman, as he outlines the likely reason that so many climbers were killed on Mount Everest in 1996.

Analogies are powerful but are rarely perfect of course, and getting back to aviation, it’s worth noting how projects can be different from aeroplane journeys.

Sometimes projects get cancelled after take-off. And this often comes as a shock to most stakeholders, on board.

You all think you’re safely underway on a nice long flight and then the sponsor suddenly plucks your plane out of the sky, so to speak.

The lesson here is not to assume that your sponsor will keep a failing project going.

Many do, that’s true, often because they fall for the sunk cost fallacy where they think,

‘I’ve sunk so much into getting this project started, I just have to finish it now’,

The result is that good money (or time) gets thrown after bad – but that obviously can’t last for long.

A strong sponsor will not be as tolerant if the project goes off track… and you might want to think about how you will respond if (or rather when) your personal projects get off track too?

Taking the greatest of care to document the ‘why’ (the purpose and benefits) of your project is the best way to start.

The Purpose and Benefits document will also help you to consider how any proposed changes (to content, costs or delivery dates, down the line) would fundamentally change the project too.

Make sense?

Do many projects fail?

Oh yes. Incredibly, most of them do!

The numbers vary by project type but, in the IT industry, for example, the failure rate can be as high as 80%.

In small business start-ups, the failure rate, according to this US data is c. 20% in year 1 rising to c.70% by year 10.

Looking at smaller scale personal projects, nearly 90% of people admit to failing on their New Year resolutions – each and every year!

If personal development projects are of more interest to you, you might also like this Insight, Seven ways to achieve more of your goals.

Human Ego is behind most project failures!

This linked article is one of many that lists the reasons why projects fail

And this ‘Dilbert’ video brings most of them to life – perfectly.

If I had to boil down all the reasons to one… I’d go with human ego.

Big, complex projects require highly competent people (experts and project managers) if they’re to succeed.

The trouble is, if your management’s capabilities are at the low end, there’s a good chance that they’ll overestimate their abilities to run this project inhouse under their personal ad hoc management and with inexperienced staff.

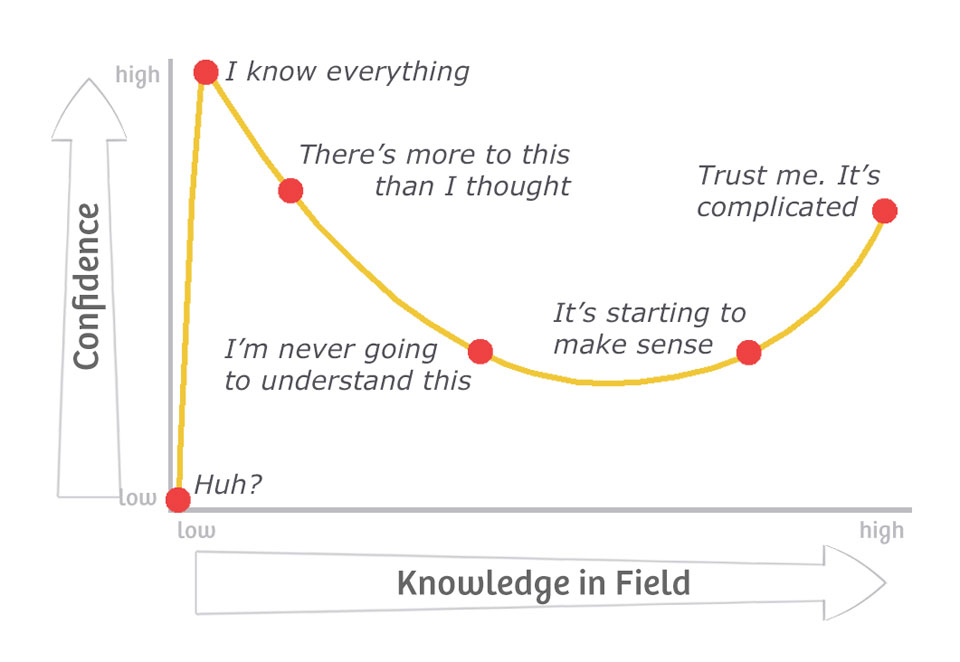

The Dunning Kruger model offers us a powerful warning signal here too.

Take a look and consider where Donald Trump sits on most issues – on this curve? As he often says, he knows more than most, nobody knows more than him etc.

Taking this further, in the excellent book ‘Business Think’ by Marcum, Smith and Khalsa. (Wiley) there’s a whole section on the need to “Leave our ego at the door”.

Here’s their excellent summary of how our ‘Ego’ can result in many undesirable transformations of strengths into weaknesses.

A useful reminder for us all, yes?

Add in some ‘hunger for a big win’ (another common of business managers) and even the strongest of projects can quickly get de-railed.

This puzzle should illustrate what I mean:

If you made a cold choice about investing in a project, which one of these would you go for:

• Project 1 – is very high risk. It only has a 10% chance of success, but if it works, will likely return c.50 % on your capital over the next two years.

• Project 2 is safer, with a 90% chance of working, but will only make you an 8% return.

Which project would you put your money into?

The logical answer is Project 2, of course.

If the chances of success can be known in advance (which they seldom can, by the way) the statistical return is 7.2% (90% of 8%) while it’s only 5% (10% of 50%) in project 1.

However, you won’t become famous or rich by investing in safe projects, so you might (like many business leaders) go for the riskier project with the higher potential return.

In fact, when it comes to personal life choices, large numbers of people take this to the extreme, following ideas promising riches to match their dreams.

What they fail to notice (or refuse to acknowledge after buying into the ‘dreams’ idea) is that its chance of success is next to nothing and it’s likely to cost a lot of time and money too 🙁

This is the hideous risk/return profile of investing time on Dream Boards and the (allegedly) Secret Law of Attraction

To see how our ego can suck us into ridiculous and dangerous ideas, watch Esther Hicks persuade a vulnerable guy that he can believe his way to winning the lottery!

Apparently, success in these multi-million dollar dreams is all about ‘getting into the vortex’.

Ughhh!

OK, I know, that’s an extreme case of our ego leading us astray, and we do need belief in the value of our project. We just need to base that belief on real benefits, which is what this step 1 is all about.

Successful project managers don’t waste time dreaming.

Their minds are grounded in the realities of the project: the tasks that need to be done; the experts required to do them; and the order in which to do them too.

They look for, report on, and seek to mitigate key risks before they become problems.

So, they’re not always popular people with business leaders, but good leaders understand that they need a great team (with a strong project manager and great subject matter experts) for project success.

We misjudge the risks – by a mile

A project is a unique endeavour with a start and endpoint. So, it’s different from business as usual (BAU) activities, and the outcomes are difficult to predict with any accuracy.

That said, in business, we tend to overestimate our chances of success, largely because we have a distorted view of the world as one with more winners than losers.

We struggle with ‘survivor bias’ which is hardly surprising, given that losers tend to hide their mistakes; we don’t see them leaving, quietly, by the back door!

You probably know Rudyard Kipling’s poem, ‘If’, which starts…

If you can keep your head when all about you

Are losing theirs and blaming it on you,

If you can trust yourself when all men doubt you,

But make allowance for their doubting too;

But do you recall his suggestion in verse 5?

If you can make one heap of all your winnings

And risk it all on one turn of pitch-and-toss,

And lose, and start again at your beginnings

And never breathe a word about your loss;

It all sounds wonderful, doesn’t it?

And I do love that poem, but perhaps it’s because so many people follow Kipling’s advice (and keep quiet about their loss) that we fail to see those losers or get any idea about risky ventures.

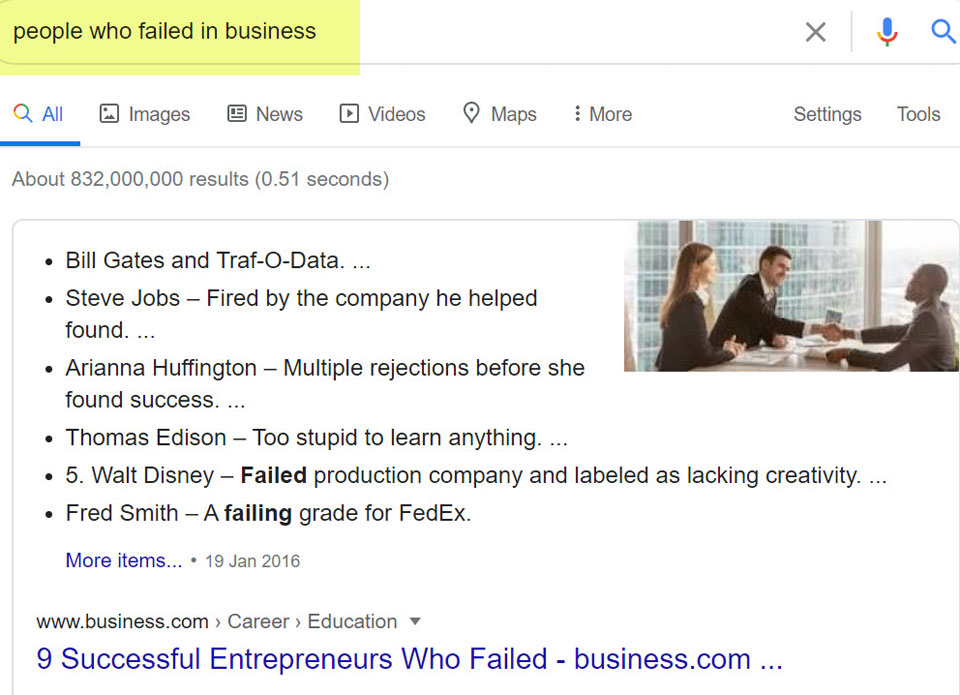

Indeed, as this shows, even if you search for ‘people who failed in business’ you’ll struggle to find any real failures

All you get are lists of people who failed at first but then, after trying again, succeeded big time.

Happy ending stories for sure… but not a helpful reflection of reality at all, is it?

Then again, it’s only a Google search of what’s on the internet, so, what did you expect – balanced truth? 😉

The real truth, as we’ve seen, is that most projects and most businesses fail.

No one wants their project to join that list, so we have to be realistic about the risks – and do what we can to mitigate them.

This is what these 10 fundamental steps are all about; improving our chances of project success.

So, let’s move on now to step 2 – which is about properly defining your project.

Step 2. Define what you’re making/changing

Yes, I know this step sounds obvious, but you’d be amazed at how many projects fail at this early stage – with a poorly defined new proposition or service enhancement.

What often happens is that the boss (Alan for example!) comes up with an idea for some ‘New Thing’, and that’s the end of any doubts about it.

Never mind getting a handle on what, precisely this ‘thing’ is, or what features it must have, to deliver the promised benefits, before we start the project… the project has already started!

Now, everyone runs around like crazy, trying to define the ‘thing’ and implement a plan to deliver it… in the invariably unreasonable timescale given!

If you’ve not yet experienced one of these projects, you’ve been lucky. Trust me, they happen; I’ve had bosses and customers try to hand them to me and, in my younger days, was naïve enough to take them on too.

My advice to you though is to avoid these ‘super-flaky’ projects like the plague.

They’re not good for your health, or your work/home life balance, and you’re going to spend a lot of time asking yourself that question from stage 1,

‘Why am I working on this?’

If you get caught in this sort of project and can’t find decent documentation on why the project exists or what it’s trying to build, have a quiet word with the sponsor about it.

You never know, you might end up saving them a ton of money by improving, (or killing off) a duff project early on.

I’ve certainly killed off my share of those, and you might even get promoted for that!

After all, as Darwin said…

Just be sure to challenge carefully and politely, when confronted with dumb ideas.

I must admit, that’s not something I always managed back in my corporate days; I wasn’t known for suffering fools gladly – especially when asked to do so on top of a 60-hour workweek!

So, it took me a while to learn but I eventually found the best approach to challenging a dumb project idea, was to start with a gentle question to the Sponsor like,

“Please can you help me understand this project?

I’m struggling to get my head around the aims and benefits, and I think we all need an outline of the product/service”

Try not to question the wisdom of the sponsor directly – and certainly not in front of others.

Do that and the pointy ‘you’re fired’ finger might reveal itself once more!

What do you need in your proposition document?

Well, that depends on what product or service you’re making or enhancing and your subject matter experts (if they’re good) should be able to help you with this.

While every project is unique, there’s bound to be someone out there who has either project managed (or provided expert input to) a project broadly similar to yours. So, find and talk to people who’ve done the sort of thing you’re trying to do – and done it well.

As for the documents, my advice is to start at a high level.

A new car might have 1,000 pages or more of detailed specifications but you don’t want a document like that… not yet anyway.

Just start with a few headings, like those you’ll find in a ‘WhatCar’ specification.

You want to define who (of your customers, your team or both groups) will benefit from your new proposition, and what features and capabilities it must have to deliver those benefits.

If you’re aiming to transform your business with a new proposition, a business model canvass is a great place to start.

Here are the key headings for this document

Comments in italics apply to information products, So, they’re less relevant if you sell physical products.

That said, information and ‘how-to’ videos are now recognised as essential to marketing most propositions and, in many cases, physical product providers are ahead of the service sector in this regard.

What exactly is your new value proposition?

What will the customer get? What problems will this solve for them and/or what needs or wants will it fulfil?

Value proposition statements are not easy, especially on information products but essential all the same.

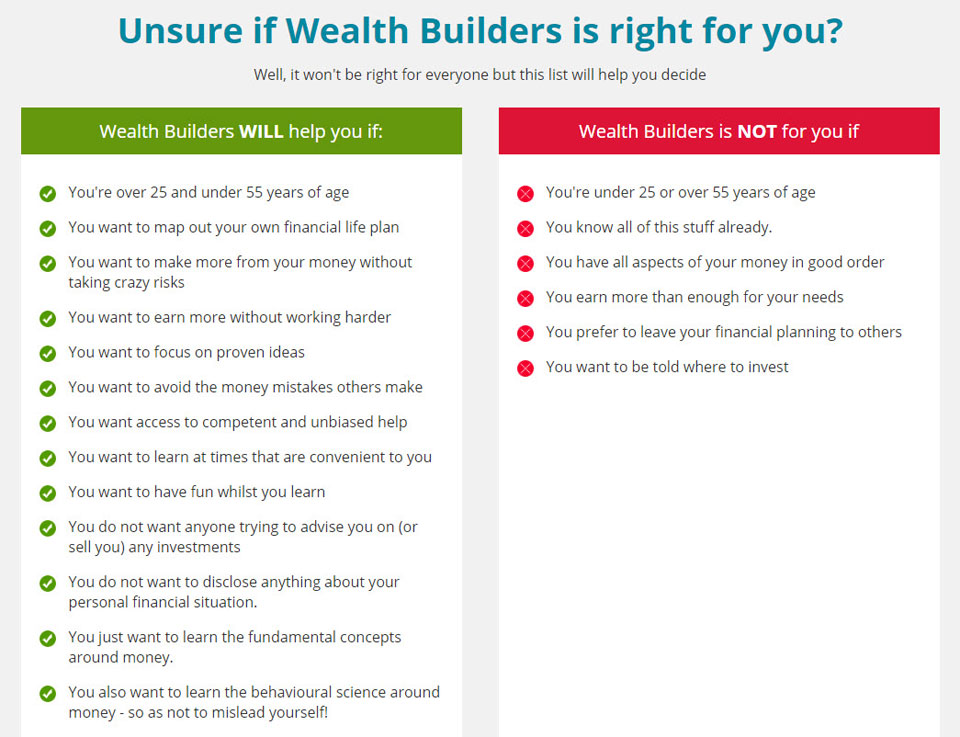

Here’s how I’ve defined my value proposition for my forthcoming WealthBuilders programme:

Proven and powerful insights for achieving more of what matters in your life; for more control of your money, better decisions on it, and more income from work, if you need it.

Hard lessons made easy and fun to learn with complex gobbledygook translated into plain English

A simple but powerful process IRATE® to define, reality test and refine your own life goals – mapped onto your own single page plan for financial freedom

Empowerment, Confidence, Control and Independence

Happy to receive feedback (+ve or -ve) on this.

Who are your target customers?

Your document needs to define who your new development will help. And, equally importantly, who won’t you help with this particular offering?

Later on, when you launch this ‘thing’, you’ll want to target your marketing to those who will benefit. So, keep these people in mind, from your project start date.

For example, for my online educational area (planned for launch later this year) the people I’m aiming to help are shown here:

If you’re a financial adviser, your target market might be very different, perhaps even the opposite, to mine, but that’s not what matters.

The essential task here is to define your market by whatever terms are relevant – whether that’s age, income, wealth, interests, pain points that need help or gains/wants that they’re looking for.

Hubspot offers a great template here if you want narrow down your buyer personas

What service levels will you offer?

Is this new development simply about one-way information giving? Or, will you also offer to answer questions of general interest?

What about open forum questions seeking personal advice? (An area to avoid around Investments) and what about personal Coaching and/or Group educational workshops?

And what will you charge at each level?

What communication channels will you offer?

How will your customers want (or post-Covid, demand) to access your information or help?

Articles on your website, Social Media, Webinars, Videos, E-mail, Books, Face to Face talks? Workshops? Telephone helpline? Online chat?

Do you want to create a community forum? Or would having a community sharing non-expert (and often misguided) opinions pose a risk to your brand?

What activities are key to deliver this proposition?

e.g. Coaching, Idea generation, Writing of blogs, videos, webinars or live workshops – and delivery of same.

What resources will you need?

Writers, videographers, Web Designers, Web Developers, Speaker trainers, and all the software and other kit that goes with this – if you plan to do a lot of this work yourself.

Get everyone on the same page

A few years back, I led Clerical Medical’s input to what was, at the time, one of the largest ever business change programmes, in the Financial Services Industry.

And I’ll never forget the acronym used by the Programme Director at the launch meeting.

On the central whiteboard, in metre-high letters, he wrote

And he said,

‘If we get this one thing right across all projects and products in this programme,

our chances of success are high…

If we get this one thing wrong, we’re doomed to fail’

What does 1VOT stand for?

One version of the truth!

With careful editing, you can get your new business proposition outlined on a single page of A4 – to help everyone on your project get on the same page – and have that 1VOT too.

Just ask me (or another proven product/propositions manager) if you need help developing these critically important starter documents for your new proposition developments.

Of course, you could always try the other way

Another acronym (or ‘initialism’) that I’ll never forget from my corporate days was that favoured by our CEO.

JFDI, or ‘Just fecking do it’ was his answer to anyone who raised concerns about his invariably unrealistic timescales on his pet projects.

And that approach to project management works just fine, when the project is no more complicated than painting the garden fence… but that’s hardly a complex project is it?

If your project is more complex than that, you can still take a JFDI approach but just change one word and…

‘Just fecking document it’

You’ll be very glad you did.

Bottom line and next steps

In this, rather chunky, Insight, I’ve shared the first two (of ten) secrets to project success.

Like many good ideas, in essence, they’re very simple.

Write down and agree with all key stakeholders:

- Why the project will benefit your organisation.

- What the new (or enhanced) proposition is – and the products or services it must contain.

The challenge is doing those things – and doing them well enough to give your project a reasonable chance of success.

Thanks for dropping in

Paul

For more ideas to achieve more in your life and make more of your money, sign up to my newsletter

As a thank you, I’ll send you my ‘5 Steps for planning your Financial Freedom’ and the first chapter of my book, ‘Who misleads you about money?’

Also, for more frequent ideas – and more interaction – you can join my Facebook group here

Share your comments here

You can comment as a guest (just tick that box) or log in with your social media or DISQUS account.

Discuss this article