Should you pay for financial advice?

And if so, what's a reasonable price?

If you’re considering working with a financial coach, planner, or adviser and are concerned about the potential cost, this Insight is for you.

This is a 10 to 20-minute read, depending on your speed.

Yes, it’s quite a long read, but we believe everyone needs to understand the (various) answers to this question.

After all, if you make a bad decision on this, it could mean:

- You pay fees for essential money guidance when there’s no need to pay anything.

- You fail to take investment advice when needed and lose thousands on expensive or bad investments or scams.

- Over the coming years, you pay thousands (or tens of thousands) in excessive fees for wealth management.

And we don’t want you to fall into any of those traps.

Let’s start with a short answer.

Yes, we believe it is worth paying for a financial coaching, planning or advice service, but only if that service delivers more value than it costs.

Of course, a good coach, planner or adviser will deliver that. Your challenge is to find the right one.

That said, some no-cost (and low-cost) guidance services are available, and one of these may provide you with the help you need now.

So, before we explore the value of broad-based financial coaching or planning, let’s examine these free and low-cost services.

When might you use the FREE money guidance services?

The good news is that free (professional) help is available if you’re unsure whether you currently receive all the state benefits you’re entitled to.

And it may surprise you that this situation applies to a great many people.

Research shows that around twenty billion pounds of benefits go unclaimed each year, either because people don’t want to claim those benefits or because they don’t realise that some benefits are available to those on average or higher incomes, especially if they look after children.

So, if you’re unsure about your entitlements, check them using any of these FREE and Government recommended services:

These organisations can answer your questions about Income-related benefits, tax credits, contribution-based benefits, Council Tax Reduction, Carer’s Allowance, and Universal Credit.

They can also explain how these benefits are calculated and how they change if you start work or change your working hours.

You should not need to seek advice about UK state benefits from any other organisation, and we urge you to report any firm or person you suspect is operating fraudulently or misleading anyone.

Sadly, some firms take advantage of people in vulnerable financial situations.

Good quality FREE advice and support is also available if you struggle to pay your priority bills (mortgage, rent, utilities, for example) or make payments on credit cards, personal loans or other debts.

In these situations, you could contact either Step Change or National Debtline.

Alternatively, for any personal money issue, contact your local Citizens Advice office, and they’ll point you towards suitable sources of help.

Finally, if you’re over 50, you also qualify for the government’s free Pension Wise service, where you can make an appointment for up to an hour to obtain general information on your pension questions.

Just be aware that the Pension Wise service won’t recommend any financial product providers or tell you how to use your pension pot or invest your money.

One hour is not enough time to develop a financial life plan, but the conversation could answer some basic questions about your pensions.

And those answers may inform your decision on whether you need advice.

What about low-cost Robo Advisers?

Are your financial foundations already firmly in place?

Have you paid off any credit/store cards or other expensive debts?

Have you insured your life (and health) and that of your partner, if you have one?

Do you have a solid financial plan in place to:

- Provide enough money for any financial dependents in the event of your death, and equip those dependents to deal with your assets (and any debts) after you’re gone.

- Provide enough money for yourself or your carers if you’re unable to work (or look after your family or home) due to a severe accident or illness.

- Provide enough money in accessible savings to pay for emergencies, like expensive repairs to your car or home or a loss of income from work.

- Build up your State Pension entitlement.

- Optimise any FREE employer contributions to your pension (or other workplace-based) savings schemes.

- Repay your mortgage (if you have one) by the time you retire, or to cope with a mortgage in retirement?

If you can answer yes to all those questions, investing some of your other money might make sense for the medium to long term.

And, a low-cost ‘robo’ advice service (or DIY investment platform, if you understand investing) might be helpful when starting your (personal) investing journey.

We’ll not assess all the low-cost investment options in this post; you can find plenty of detailed comparison tables elsewhere.

The term “Robo Advice” could mean many things, but often describes a system that offers simple investment advice and aims to reduce costs by automating the Investment fund selection process.

What does that mean – for you?

You do a lot of the work by gathering all your financial details, entering them into the Robo Adviser system, and completing their ‘Attitude to Risk’ questionnaire online.

Also, as far as we can tell, most Robo advice systems require you to decide which financial product suits your circumstances.

Good financial product selection is vital but not simple, as some ‘money experts’ prove when they offer poor advice on TV.

So, we offer this separate series of Insights to help you with that question.

You may also wish to seek qualified and personal guidance on the right financial products before buying them through a Robo Adviser or other online system.

Assuming you know which financial product is right for you, the robo-advice system will suggest an investment portfolio (or fund) from its limited range.

Typically, the system provides an online platform (and a mobile app) for you to invest in those products and funds and monitor and manage your accounts.

If you’re genuinely capable of making sound investment choices on your own, you could save money* by going without the Robo Advice element and buying your investments without any advice on one of the leading DIY investment platforms.

* The amount you’d save by not taking Robo advice varies according to which providers you compare.

By taking a DIY approach, we estimate you may save between 0.3% and 0.6% each year on the value of the monies you hold on the platform.

Of course, this Insight is about the value of advice – assuming you need some. So, we’ll not dive deeper into DIY investment platforms here.

Do we like Robo Advice systems?

A sound Robo Advice system can potentially help people who:

- Know the best financial product for their particular financial life goals.

- Have financial needs that can be met by the financial products and funds offered.

- Are uncomfortable making investment decisions on their own.

- Don’t feel they need a full advice service from a human adviser.

However, as stated above, Robo Advisers typically offer limited (or no) financial planning or product selection advice and generally provide a restricted product and fund range.

So, in general, we prefer an approach that gives you access to a full financial planning service, a wide range of products and funds, and real conversations with qualified human advisers.

You can always put the (say, 0.45% p.a.) fee you’d pay for Robo Advice towards a full financial planning service if that’s right for you.

The additional cost of dealing with humans is not always significant, but the extra value can be.

Features of Robo advice services to check

If you still wish to explore taking Robo Advice, check that the provider you’re considering is regulated by the Financial Conduct Authority (FCA).

Being regulated should mean that any complaint you make about service is taken seriously by the Financial Ombudsman Service. It also means you can claim compensation (up to the Financial Services Compensation Scheme limit) if you lose money due to failings by the provider.

Note: The compensation scheme does not protect you from investment losses on a Robo Advice platform (or full advice service) if those losses arise from market-wide asset value falls.

So, it’s vital that the funds you invest into match both your attitude to risk and your capacity to take investment risks on each of your goals.

And we’re concerned about how Robo Advice services deal with the ‘capacity for risk’ question.

In any event, we urge you to search the FCA’s online register of providers to ensure your chosen provider is registered. And double check that the website you use is not a scam copy of the legitimate site.

Beyond that, we suggest you check that the Robo adviser you’re considering:

- Offers a sufficiently wide range of financial products (tax wrappers), so you can place your money in the most suitable product for your circumstances.

- Offers enough investment funds (and securities if you need that) for you to invest in what’s right for you – including any sustainable investments if those are important to you.

- Applies a robust process for checking your attitude to risk and adjusts that result to take account of your capacity for risk – on each of your financial life goals.

- Saves you enough in fees to make it worthwhile giving up access to a qualified human adviser.

You’ll also want to consider what other investment opportunities you have.

For example, what free money (or share discounts) are available on your pension or share save scheme at your place of work?

To be clear, we do see a need to streamline the financial planning process with online solutions that add value and keep costs down. And the best financial advisers use systems that deliver these improvements to you.

You just need to be aware of the advice-scope limits of Robo systems and consider the benefits carefully.

Could financial coaching be right for you?

Working with a financial coach may be right for you if you want a genuine conversation with a human instead of automated chats with a robot, although you could combine both services.

Working with a financial coach may be right for you if you want a genuine conversation with a human instead of automated chats with a robot, although you could combine both services.

Human involvement is vital if you want an in-depth exploration of your personal financial situation – and to design a plan that connects your money to your hopes for the future.

There is enormous value in having an experienced and qualified person listen, understand and react appropriately to what you say (and feel) about money matters.

Despite recent advances in artificial intelligence, we’re unaware that machines have cracked the code for doing that!

Despite recent advances in artificial intelligence, we’re unaware that machines have cracked the code for doing that!

A good financial coach will listen more than they talk. They offer you a quiet space to talk and think through your financial concerns and ambitions.

If the coach is well-trained, they should be able to:

- Help you think through and focus on the areas of your money management that need attention. And challenge you to attend to those areas.

- Point you to relevant and valuable information on various financial matters.

- Help you explore (and understand) the main financial products – and help you avoid the big pitfalls – especially around Scams.

- Support and encourage you to take more control of your money.

Good financial coaches can also mentor you on financial matters while providing (generic) guidance and resources to help you make your own financial decisions.

Organising your money tasks (and your money mind) can be a helpful introduction to financial planning. And financial coaches generally charge a bit less than regulated financial advisers.

Just be aware that unless the coaching is part of a regulated advice service, the coach cannot offer investment recommendations.

Could financial planning and advice be right for you?

A regulated financial advice service offers many potential benefits:

You receive specific recommendations on the financial products (insurance, investment or pension) to set up and where to place new (or transfer existing) monies.

You also receive advice on the investment funds to hold within the investment and pension products, on which you take advice.

The recommended financial products should offer good value for money – which might save you significant costs compared to buying those products yourself.

For example, arranging your insurance through an adviser might save you several hundred pounds (over the policy term) on life and health insurance products alone.

Any recommendations should also reflect your personal needs and goals, financial circumstances, and attitude to (and capacity for) investment risk.

You can also access a complaints process and compensation if you’re found to have received bad advice.

And, while there should be no need to complain, it’s worth remembering that you do not have this protection if you advise yourself.

Some advisers also offer financial education and coaching sessions, but this varies. So, if you value these services, ask your adviser about them.

Finding the right advice – at a fair price

There are no simple, golden-rule answers to the question of what’s a fair price for advice.

A fair price for advice depends on the expertise you need and the effort required from those who help you understand your current situation and help you design and implement your unique financial plan.

For example, an hourly charging fee-based adviser specialising in the complex financial needs of business owners or high net-worth individuals might charge between £250 and £350 per hour for their advice.

These are similar to the fees you’d pay for complex legal advice, and we suggest you get good quality advice in both of these areas.

If your finances are straightforward, you may be able to arrange a financial review and set up any strategies or financial products you need for around £175-£200 per hour, which, research shows, is the typical range for general financial advice.

Just be aware that fee-charging structures can vary quite a lot.

Some advisers charge by the hour, some for the project of work you agree upon, while many charge a small percentage of the amounts you place under their advice – with a separate ongoing fee if you agree to their ongoing services.

Some firms also advise in specialist areas that others can’t advise you on, and some firms state that you must have a minimum investment amount (including your pension funds) before you can access their services.

So, finding a suitable adviser for your needs can be confusing.

That said, you can find out which advice areas are covered by the firm you’re considering by searching one of the adviser search engines listed here:

- The Money Helper retirement adviser directory

- The Personal Finance Society

- Unbiased

- Vouched for

- Society of Later Life Advisers for an accredited later-life adviser.

Then, with a short list of possible advisers, you can usually arrange an initial meeting free of charge to learn more about their services and fees.

Focus on value – and avoid excessive fees.

The real value of an advice service comes from the work done with you to build a plan personalised to your circumstances, needs, and ambitions.

So, be aware that financial advice fees are separate from those for administering your financial products and managing your investments inside those products.

Of course, a good adviser will ensure you receive good value advice and service in each of those areas. And you’ll gain enormous value from recommendations of investment funds that match your attitude and your capacity for investment risk – on each of your goals.

Does it matter if you pay (a bit) too much?

The point about fees is to pay a fair amount for the services you receive. The amount of work and the complexity of the advice will vary according to your needs.

You should, however, be aware of the potentially drastic effect of (seemingly) small (say, 1%) excessive charges on your money over time.

We use a 1% figure because such (extra) fees are not uncommon. And that’s what more expensive wealth managers charge when compared to better value advisers.

The question we want to help you consider is this:

What exactly is the cost of paying, say, 3% p.a. (of your funds under advice) for good quality financial planning and wealth management – if you could enjoy the same service for a total fee of 2% p.a.

These charts answer that question.

This first chart shows what an unnecessary 1% extra charge would cost you over various time periods on a £500 per month investment savings plan (pension or ISA, for example).

See how those unnecessary charges add up to around £10,000 on a 15-year (regular) investment plan or £60,000 over 30 years.

Please note: these figures are adjusted for inflation, so that’s £60,000 in today’s money terms.

Of course, you can use this chart to see the excessive fees on larger or smaller savings amounts.

For example, if you’re saving £100 per month (one-fifth of the £500 in the example above), then 1% overcharging would cost you around £12,000 (one-fifth of £60,000) in today’s money terms over 30 years.

What’s the picture for lump sum investments?

This second chart shows how a simple 1% excessive charge would eat into the value of a lump-sum investment over time.

You can see that an unnecessary extra charge of just 1% p.a. adds up to c. £40,000 over 20 years, assuming a £100,000 initial investment.

And, these numbers apply regardless of whether the investment product is a Stock and shares ISA, personal pension, mutual fund/unit trust, or any other type of investment product.

As before, you can use this chart to see the effect of overcharging on larger or smaller investments.

For example, on an investment of £1 million (ten times the example above), an unnecessary extra charge of 1% p.a. would mount up to £400,000 (10 times £40,000) in today’s money terms over 20 years.

Whether it’s £40,000 or £400,000, we see that as your money – and we’re quite sure that you don’t want it wasted on excessive charges.

Don’t underestimate the work of planning your money effectively

What’s your conclusion so far?

What’s your conclusion so far?

Perhaps you’re thinking:

‘to hell with any of these charges,

I’ll sort my finances out myself’

And that might be just fine.

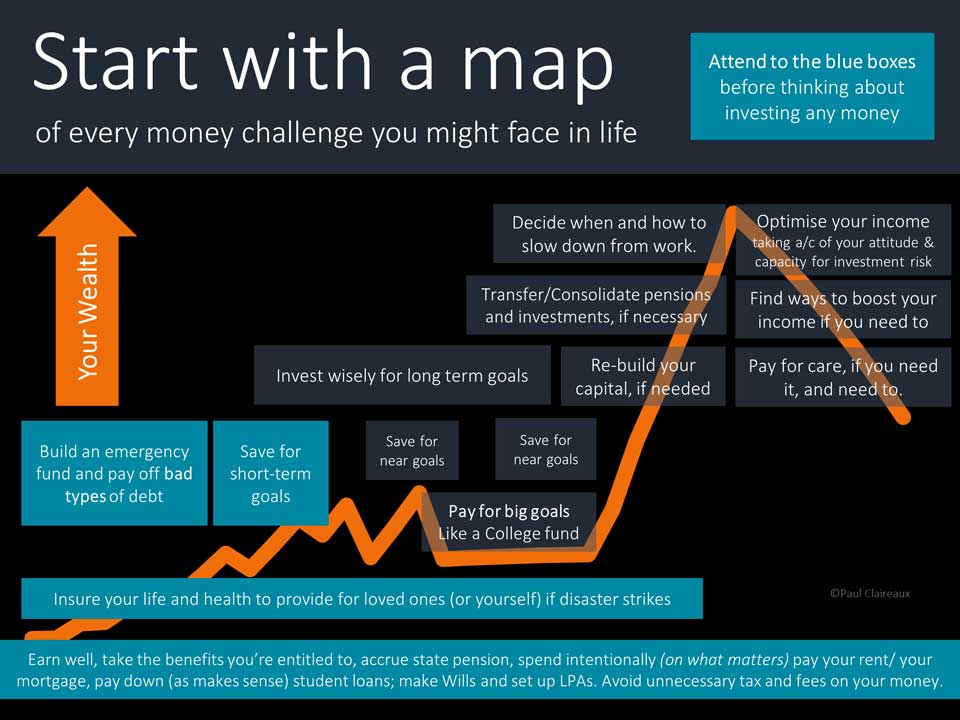

However, if your finances are even mildly complicated (and not yet well organised), you may have considerable work to do.

You’ll need a good picture of what you have now – and to design a plan to deal efficiently (without wasting money on charges or taxes) with the many money challenges you might face over time.

This picture gives you a sense of those challenges.

Thankfully, you’ll not have to deal with all those things at the same time, but it’s still hard work to deal (effectively) with each challenge as it comes along.

And, if you don’t have an adviser nudging you to save and invest early enough, it can quickly become too late to achieve your original goals.

So, like the last-minute savers in this picture (who want to catch up with those who started early on the steady path), you might be tempted to take more investment risks with your money.

That’s a common reaction – but precisely the wrong thing to do.

Of course, you may be extremely capable – and know how to sort out everything in the map above:

- Without overpaying for the financial products.

- Without overpaying for advice.

- Without paying unnecessary taxes.

- Without taking excessive investment risks.

However, most people with surplus income, capital (or pension funds) to invest (or other financial planning needs) find professional help enormously valuable.

Interestingly, many financial experts work on their finances with the help of other financial planners – and there are two reasons for this.

First, it’s almost impossible to be objective about our personal situation – and stay alert to our own behavioural biases.

(We’ll cover behavioural biases in more detail in future.)

Second, if you have a life partner with little or no expertise in personal finance, you may want to ensure they have someone trustworthy to turn to for advice – for that (unknowable) time when you face long-term illness or your days are done.

So, regardless of your expertise, if your circumstances suggest that you (or your partner) could benefit from professional advice, we urge you to find a good adviser.

You’ll feel better when you’re clear about which financial tasks you need to address – and you’re making progress on them.

I hope that’s helpful.

Thanks for dropping in

Paul

For more ideas to achieve more in your life and make more of your money, sign up for my newsletter here

You can comment as a guest (tick that box) or log in with your social media or DISQUS account, at the base of this page.

You can comment as a guest (tick that box) or log in with your social media or DISQUS account, at the base of this page.

For financial advisers, planners and coaches

This educational insight is one of many we’re creating for you to use in your business, under lifetime licences.

These works aim to help people make sound financial decisions and recognise the value of professional advice.

You can, of course, brand these insights to your business style, and add your firm’s calls to action.

For financial advisers and coaches

To use this or other educational insights in your business.

Discuss this article